Plan for Unit 2, Investor Preferences

Complete Part Two of class project

You will understand the concept of utility. You will learn how to

evaluate different investment options.

Use return data from Jan 2010 to Dec 2016. You will need the last

year to evaluate out-of-sample performance.

The risk free rate is what you computed in Unit 1.

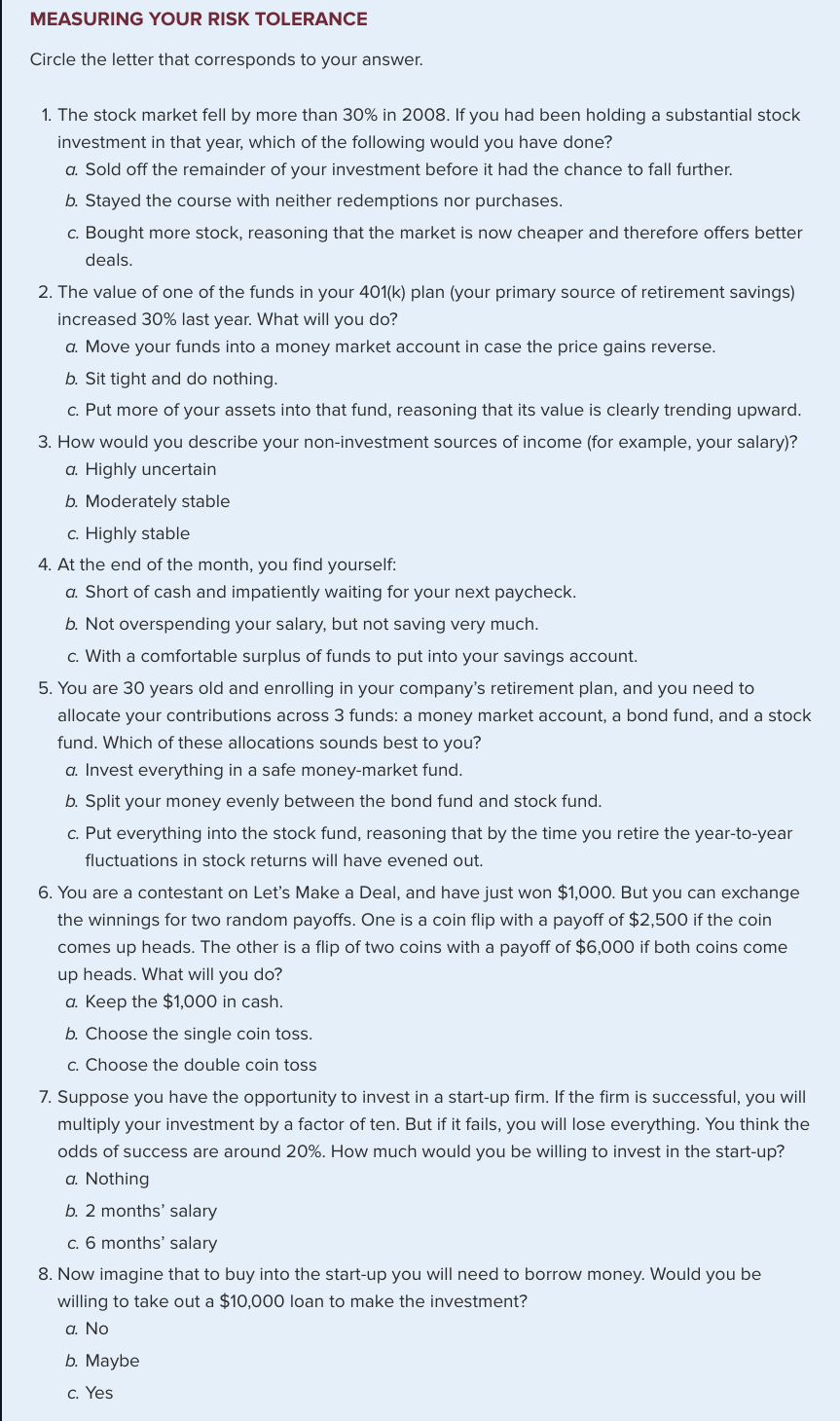

Measure your risk tolerance and your utility

- Do the survey on page 163(20min):

Each answer (a) is 1 point, each answer (b) is 2 points, each answer (c)

is 3 points.

- If you have between 8 and 14 points assign a risk aversion

coefficient of 9. If you have 15, 16, 17, or 18 points, assign a risk

avertion coefficient of 3, and if you have more than 18 points, assign

a risk aversion coefficient of 1. (20min)

- Plot all nine ETF portfolios (use scatter plot in excel) on the

same graph. The Y axis will be return, the X axis standard deviation.

(20min)

- What is Mean-Variance Criterion? What is portfolio dominance? Are there

any industry portfolios on the graph which are dominated by other

portfolios? Describe. (30min)

-

What is your utility as an investor holding each industry portfolio

separately. Which portfolio would you prefer. (40min)

- Plot your indifference curve across this preferred portfolio, on

the same graph on which you plotted all nine portfolios. (50min)

- Together with your teammates, plot the individual team member

indifference curves on the same graph, each indifference curve going

through across each member's preferred portfolio. (40min)

You can invest in one ETF and the risk free rate

- If you can allocate your money between one ETF and the risk free

rate, which ETF will you choose? Why?(30min)

- On the graph on which you have been working, add the best capital

allocation line?(30min)

-

What proportion of your investment should you allocate to the risk

free asset and what proportion should go to the best risky asset (ETF)

that you determined to maximize your utility?(50min)

-

What is your utility at this optimal allocation point? How can you

show that this is indeed the optimal point? (30min)

-

How does your utility compare to the case when there was no risk-free

asset?(20min)

-

On the same graph that you have been working with, plot your new

indifference curve.(30min)

Put together the following summary, based on all the

calculations you've done so far: Compare the utility that

you had when you invested in(50min):

- Just one ETF.

- Just one ETF combined with the risk-free asset.