| CRN | Subj | Crse | Sec | Title | Days & Time | Date (MM/DD) | Location | Office Hours |

|---|---|---|---|---|---|---|---|---|

| 16805 | MBA | 706 | 001 | Investments | W 7:20pm - 10:00pm | 08/19-10/09 | Fairfax: Buchanan 001 | By appt: Book |

| This course is about portfolio management and asset pricing. The material focuses on institutional investing, although the course is also relevant for individuals. The class aims to provide an understanding of strategies and risk management tools necessary for the management of fixed income and equity portfolios. In particular, the class material covers asset allocation, risk and return trade-offs, diversification, asset pricing, portfolio performance evaluation, and the theory of market efficiency. Upon successful completion of this course students will be able to (1) evaluate and explain the risk and return trade-offs in finance and (2) conduct research necessary to construct, manage, and evaluate equity/fixed income portfolios and evaluate their performance. |

| Completion of MBA core or permission of instructor. Prerequisite enforced by registration system. Students are expected to be familiar with basic economics and statistics. |

|

|

The course grade will be based on a score of 1000 points. The grade distribution is as follows: 930-1000 (A), 900-929 (A-), 860-899 (B+), 800-859 (B), 700-799, C. The final grade will be based on a set of practice problem sets (total of 200 pts), a team project mainly developed in class (five parts totaling 600 pts) which will require teams to set up, manage, and evaluate the performance of a diversified portfolio, a Bloomberg Portfolio Management tutorial (150 pts), and class participation (50 pts). The problem sets will have a carefully selected number of questions and will be administered online on Blackboard. You will be able to access each problem set within a specified period of time and will be able to work on it at your convenience. You will also have an opportunity to work on some of the problems in class. For the in-class project, you will join a team. The first task in the project is to examine an existing portfolio through Bloomberg. You will consider this benchmark portfolio to be a passive investment choice available to your clients. You and your team will put together a portfolio which is similar to the benchmark (has the same asset classes). However, you will actively manage this portfolio, performing asset allocation, stock selection, and portfolio performance evaluation tasks. Your goal will be to outperform the benchmark fund. You will be doing quantitative and qualitative analysis using one or more of the following applications: Python, Office365 (the MS cloud) docs, Google sheets, Bloomberg. In Bloomberg, you will extensively be using the PORT analysis tool. You will present your results in class. More details about the project are available through the web links in the class schedule table. Another component of the grading will be Bloomberg Market Concepts (BMC), a Bloomberg tutorial. Very recently, BMC has been divided in three sections for a more customized experience: Core Concepts, Getting Started on the Terminal, and Portfolio Management. I have made the BMC Portfolio Management tutorial a part of this course. When you sign up for it, use the following code: BS24PLTCZ6. Upon completing this tutorial you will receive a certificate.

|

| By registering for this class, students agree to abide by the honor code, which describes the standards of conduct, academic violations, and the treatment of academic offenses. The Honor Code states that all students "pledge not to cheat, plagiarize, steal, or lie in matters related to academic work." Visit the Full Honor Code to read more about the GMU academic integrity code. School of Business Honor Code guidelines are posted at the end of this syllabus. |

| Wk | Date | Class Topic | Related Course SLO | Learning goal for class | Learning value | Related AT | Related LST | Prep or Feedback |

|---|---|---|---|---|---|---|---|---|

| 1 | Aug 19 | Risk and Return (Slides) | Understand the different 'incarnations' of return (expected, historical, arithmetic and geometric mean, annual percent rate, effective rate ) |

LO5-1 Understand interest rates and compute various measures of return on multi-year investments. LO5-2 Use data on the past performance of stocks and bonds or scenario analysis to estimate expected returns and standard deviations. Compute and compare arithmetic and geometric mean returns. |

Essential to describe financial performance and wealth generation. This is how investors make expectations. Needed for comparing investment choices. |

Table 5.1 (excel)

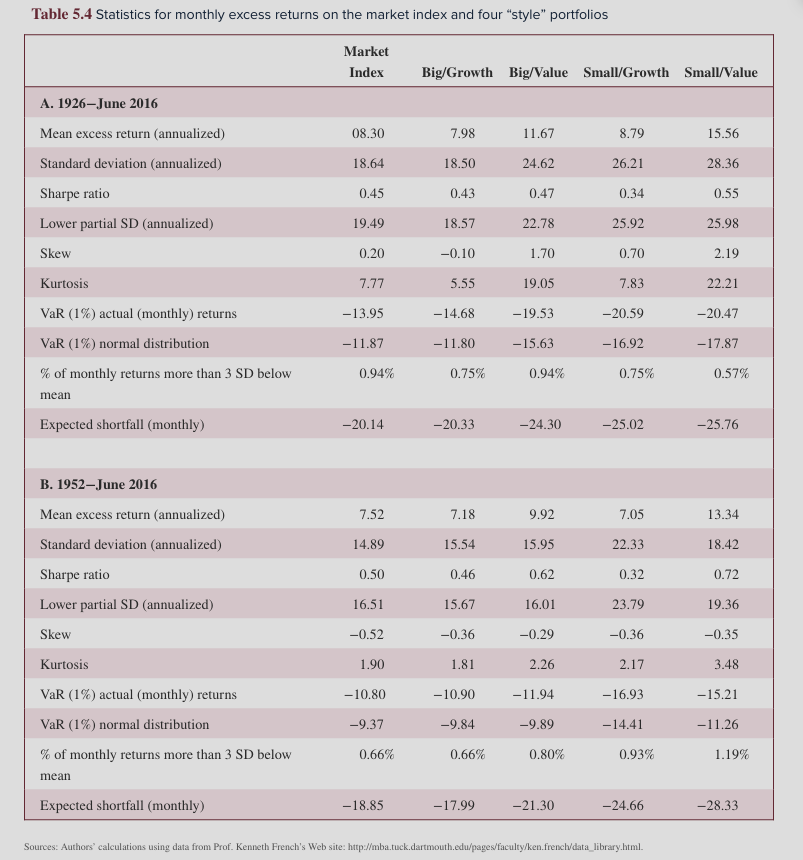

pr7.15 (excel) Spreadsheet 5.1 (excel) Spreadsheet 5.2 (excel) Excel Return Data Ch.5– compare with the historical performance reported in BKM Table 5.4 |

BB PS1 Q1[1]

BB PS1 Q2 BB PS1 Q3 BB PS1 Q4 BB PS1 Q5 BB PS1 Q7 |

Slides 1–19 Slides 20–33 |

| |

Understand what the meaning of risk is in finance |

LO5-3 Understand the normal distribution and how VAR is related to it. Understand and evaluate different measures of risk. LO5-4 Use the Sharpe ratio to evaluate the investment performance of a portfolio and provide a guide for capital allocation. |

The normal distribution helps us estimate probabilities and assess risk | |

BB PS1 Q6 BB PS1 Q8 |

Slides 35–57 Slides 57–64 are optional. |

||

| 2 |

Aug 26 |

Plan for Part 1 of the Project |

Work with real financial data |

|

Corresponding project items: |

|

||

| 3 | Sep 2 | Capital Allocation to Risky Assets | Understand the finance concept of utility Learn how to evaluate different investment options. |

LO6-1 Estimate or infer risk aversion, compute utility values of investment choices LO6-2 Be able to compute the investor's allocation in one passive risky portfolio and a risk-free asses. Use and construct the Capital Allocation Line. |

It shows how investors make choices |

pr6.4 (excel) pr6.10-12 (excel) pr6.5 (excel) pr6.13 (excel) pr6.21 (excel) pr7.16 (excel) |

Solve P2 Q9 |

Slides 1–14 |

| |

|

|

LO6-3 Determine the optimal position in the complete optimal portfolio. Build indifference curves. LO6-4 Determine the equivalence of two risky choices, as well as their certainty equivalent. Understand diminishing marginal utility. |

|

pr6.14-19 (excel) pr6.22 (excel) pr6.24 (excel) pr6.26 (excel) tb6.6 (excel) pr6.29 (excel) | Solve BB P2 Q1–3, Q5, Q8 Solve BB P2 Q4, Q7 Solve P2 Q6 |

Slides 15–27 Slides 28–52 |

|

| 4 | Sep 9 |

Project part 2 |

|

Determine investor choices among the 9 ETFs |

Corresponding project items: |

|||

| 5 | Sep 16 | Optimal Risky Portfolios | Understand the power of diversification |

LO7-1 Calculate covariance and correlation. Compute portfolio mean and variance. LO7-2 Show how covariance and correlation affect the power of diversification to reduce portfolio risk. LO7-3 Calculate the optimal risky portfolios and construct the efficient frontier. LO7-4 Add the risk-free asset to the set of efficient portfolios and determine the optimal complete portfolio |

|

pr7.4 (excel) pr7.5 (excel) pr7.7 (excel) pr7.8 (excel) pr7.9 (excel) pr7.12 (excel) |

BB BB P3Q2 BB BB P3Q1 BB BB P3Q3 BB BB P3Q4 BB BB P3Q5 |

Slides 1–8 Slides 9–15 Slides 16–21 Slides 22–40 Slides 41–57 are optional |

| 6 | Sep 23 | Project part 3 |

Estimate the efficient frontier with the 9 ETF portfolios |

Corresponding project items: |

||||

| 7 | Sep 30 | The Capital Asset Pricing Model (CAPM) | Understand that only systematic risk is priced |

LO9-1 Use the implications of capital market theory to estimate security risk premiums. LO9-2 Construct and use the security market line. |

We can value stocks. We can identify mispriced stocks | |

|

|

| |

|

Project part 4 |

|

Asset pricing with the CAPM |

|

Corresponding project items: |

BB P4Q7–9 |

|

| 8 |

Oct 7 |

Portfolio Performance Evaluation | |

LO24-1 Compute risk-adjusted rates of return, and use them to evaluate investment performance. LO24-2 Determine which risk-adjusted performance measure is appropriate in a variety of investment contexts. |

Excel Template and Solutions Ch.24 |

|

|

|

| |

|

Bloomberg Webinar Slides on PORT |

|

LO24-3 Apply style analysis to assess portfolio strategy. LO24-4 Decompose portfolio returns into components attributable to asset allocation choices versus security selection choices. LO24-5 Assess the presence and value of market-timing ability. |

|

Excel Performance Measurement Ch.24 |

|

|

| Project part 5 |

Performance evaluation |

|

Corresponding project items: -items 1-2 -items 3-4 -items 5-8 |

|

|

[1] You need to be logged in Blackboard to access this link

{kind=link}